2015 Annual Report: Additional Opportunities to Reduce Fragmentation, Overlap, and Duplication and Achieve Other Financial Benefits

GAO-15-404SP

Published: Apr 14, 2015. Publicly Released: Apr 14, 2015.

Skip to Highlights

Highlights

Improving Efficiency and Effectiveness

GAO's 2015 Annual Report identified 12 new areas of fragmentation, overlap, and duplication in federal programs and activities. GAO also identified 12 new opportunities for cost savings and revenue enhancement. Related work and GAO's Action Tracker—a tool that tracks progress on GAO's specific suggestions for improvement—are available here.

What GAO Found

In its 2015 report, GAO presents 66 actions that the executive branch or Congress could take to improve efficiency and effectiveness across 24 areas that span a broad range of government missions and functions.

- GAO suggests 20 actions to address evidence of fragmentation, overlap, or duplication in 12 new areas across the government missions of defense, health, income security, information technology, and international affairs.

- GAO also presents 46 opportunities for executive branch agencies or Congress to take actions to reduce the cost of government operations or enhance revenue collections for the Treasury across 12 areas of government.

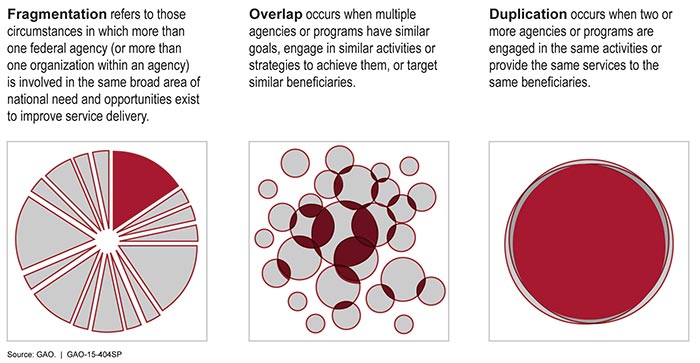

Defining Fragmentation, Overlap, and Duplication

Recommendations

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress may wish to permanently rescind the remaining $600 million balance of the U.S. Enrichment Corporation (USEC) Fund. | As of March 2023, Congress had not passed legislation to permanently rescind the entire balance of the USEC Fund, as GAO suggested in April 2015. However, Congress has passed legislation to transfer all remaining balances in the USEC Fund to the Uranium Enrichment Decontamination and Decommissioning Fund, which is used to help pay for cleanup costs at the nation's former enrichment plants. Specifically, in December 2020, Congress passed the Consolidated Appropriations Act, 2021, which included a provision directing that $291 million of the balances in the USEC Fund be transferred to and merged with the Uranium Enrichment Decontamination and Decommissioning Fund. Pub. L. No. 116-260, div. D, tit. V, SS 506, 134 Stat. 1182, 1379 (2020). In addition, in March 2022, Congress passed the Consolidated Appropriations Act, 2022, which the President signed March 15, 2022. The act included a provision directing that $841 million of the balances in the USEC Fund be transferred to and merged with the Uranium Enrichment Decontamination and Decommissioning Fund. Pub. L. No. 117-103, 136 Stat. 49, div. D, tit. III, SS308 (2022). On March 24, 2022, $841 million was transferred from the USEC Fund to the Uranium Enrichment Decontamination and Decommissioning Fund, leaving a remaining balance of approximately $600 million in the USEC Fund. Finally, in December 2023, Congress passed the Consolidated Appropriations Act, 2023, which the President signed into law on December 29, 2022 (Pub. L. No. 117-328). The act included a provision that all remaining balances in the USEC Fund be transferred to and merged with the Uranium Enrichment Decontamination and Decommissioning Fund. In January 2023, all remaining balances in the USEC Fund, totaling approximately $616.7 million, were transferred out of the USEC Fund. |

Full Report

GAO Contacts

Public Inquiries

Topics

MedicareMedicaidEarned income tax creditClaims paymentsAgency evaluationsCompliance oversightCost savingsGovernment efficiencyHospitalsManaged health care