2014 Annual Report: Additional Opportunities to Reduce Fragmentation, Overlap, and Duplication and Achieve Other Financial Benefits

GAO-14-343SP

Published: Apr 08, 2014. Publicly Released: Apr 08, 2014.

Skip to Highlights

Highlights

Improving Efficiency and Effectiveness

GAO's 2014 Annual Report identified 11 new areas of fragmentation, overlap, and duplication in federal programs and activities. GAO also identified 15 new opportunities for cost savings and revenue enhancement. Related work and GAO's Action Tracker—a tool that tracks progress on GAO's specific suggestions for improvement—are available here.

What GAO Found

In its 2014 report, GAO presents 64 actions that the executive branch or Congress could take to improve efficiency and effectiveness across 26 areas that span a broad range of government missions and functions.

- GAO suggests 19 actions to address evidence of fragmentation, overlap, or duplication in 11 new areas across the government missions of defense, health, income security, information technology, and international affairs.

- GAO also presents 45 opportunities for executive branch agencies or Congress to take actions to reduce the cost of government operations or enhance revenue collections for the Treasury across 15 areas of government.

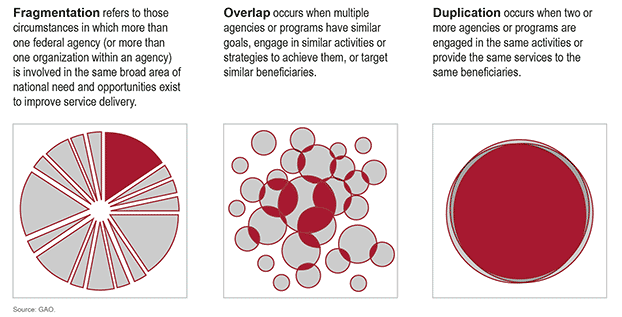

Defining Fragmentation, Overlap, and Duplication

Recommendations

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider passing legislation to require the Social Security Administration (SSA) to offset Disability Insurance (DI) benefits for any Unemployment Insurance (UI) benefits received in the same period. | Two bills in the current Congress have been introduced that could address this matter. Specifically, H.R. 7104 and S. 3648 were both introduced in January 2026. Section 4 of each bill would prohibit the payment of Social Security disability benefits when the individual is eligible for unemployment compensation. Similar bills were introduced, but not enacted, in the 114th, 117th, and 118th Congresses. According to the Office of Management and Budget, implementing such legislation could save $2.18 billion over ten years for the Social Security Disability Insurance program. | |

| Unless the Department of Energy (DOE) can demonstrate a demand for new Advanced Technology Vehicles Manufacturing (ATVM) loans and viable applications, Congress may wish to consider rescinding all or part of the remaining $4.3 billion in credit subsidy appropriations. | In December 2020, Congress passed and the President signed legislation rescinding part of the ATVM program's remaining credit subsidy appropriations, as GAO had suggested in April 2014. Specifically, the Consolidated Appropriations Act, 2021 rescinded about $1.9 billion of the ATVM program's remaining $4.3 billion in credit subsidy appropriations (Pub. L. No. 116-260, 134 Stat. 1182, 1367 (Dec. 27, 2020)). Congress now has the opportunity to use the funds for other priorities. |

Full Report

GAO Contacts

Public Inquiries

Topics

Defense operationsDisability benefitsExecutive agenciesFederal agenciesFiscal policiesInformation technologyInternational relationsPaymentsProductivity in governmentProgram evaluationProgram managementTaxesDuplication of effortProgram goals or objectivesSavings estimates