Death Services: State Regulation of the Death Care Industry Varies and Officials Have Mixed Views on Need for Further Federal Involvement

Highlights

What GAO Found

The extent to which the federal and state governments regulate the death care industry—funeral homes, cemeteries, crematories, pre-need funeral plans, and third party sales of funeral goods—varies, as does the extent to which regulation has changed since GAO last reported on the regulation of the death care industry in 2003. The Federal Trade Commission (FTC) continues to annually conduct undercover shopping at various funeral homes to test compliance with the Funeral Rule. Of the over 2,400 funeral homes that the FTC shopped since 1996, the FTC reported an overall compliance rate of about 85 percent. With respect to state regulation, consistent with GAO’s findings in 2003, the way in which states regulate the industry varies across industry segments and states. Also, the extent to which state regulators reported that they had specific rules or regulations for each industry segment in both 2003 and 2011 varied. Most consistent across states in both years was reporting that there were specific rules or regulations for funeral homes (94 and 95 percent in 2003 and 2011, respectively). In contrast, 77 percent of state regulators of cemeteries reported that their states had specific rules or regulations for cemeteries in 2003, and 88 percent reported this in 2011. Certain state regulators also reported that their states made various statutory or regulatory changes since 2003, primarily to clarify legislation or regulation or to enhance consumer protections, and that they believe these changes strengthened their regulatory program to varying degrees. State regulators reported that these changes came about for a variety of reasons, including accounts of desecration of human remains or proposals from state agencies and industry groups.

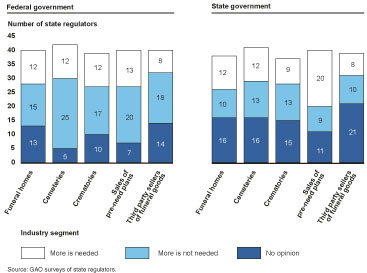

State regulators’ views on the need for additional federal and state regulation of the industry varied, as shown in the figure below.

The FTC provided technical comments, which GAO incorporated where appropriate.

Why GAO Did this Study

Media reports have identified instances of desecration of graves and human remains at cemeteries, and in one instance, reported that bodies were removed from graves and the sites resold. Allegations have also surfaced about the mismanagement of pre-need plans that are designed to provide consumers the opportunity to fund funeral and cemetery arrangements before they are needed. The FTC’s Funeral Rule requires that, among other things, funeral providers give consumers lists that disclose the cost of funeral goods and services before they enter into funeral transactions. Proposed legislation introduced in March 2011 would increase the federal government’s role in regulating the industry by, among other things, requiring that the FTC regulate aspects of cemetery operations. GAO was asked to review the regulation of the death care industry. This report discusses (1) how federal and state governments regulate the industry and how regulation has changed since 2003 and (2) state regulators’ views on the need for additional regulation.

GAO reviewed FTC’s Funeral Rule and interviewed officials representing the FTC and national industry and consumer associations; surveyed state officials to gather data on state regulation of the death care industry; and, where possible, compared the results of the 2011 surveys with those of similar surveys GAO conducted in 2003. The response rate for our 2011 surveys ranged from 78 to 84 percent. GAO also reviewed laws and regulations. GAO is not making any recommendations in this report.

For more information, contact William O. Jenkins, Jr. at (202) 512-8777 or jenkinswo@gao.gov.