Issue Summary

The federal government spends trillions of dollars each year to carry out its operations, including national defense, health care, transportation, and interest payments on the federal debt. Congress passes laws that authorize agencies to spend federal dollars for certain purposes. This includes mandatory budget authority, which is generally driven by eligibility rules and benefit formulas, and discretionary budget authority, which is generally provided by annual appropriations acts. Mandatory spending includes programs like Medicare and Social Security, while discretionary spending supports agency programs and operations including most spending on defense, education, housing, and energy.

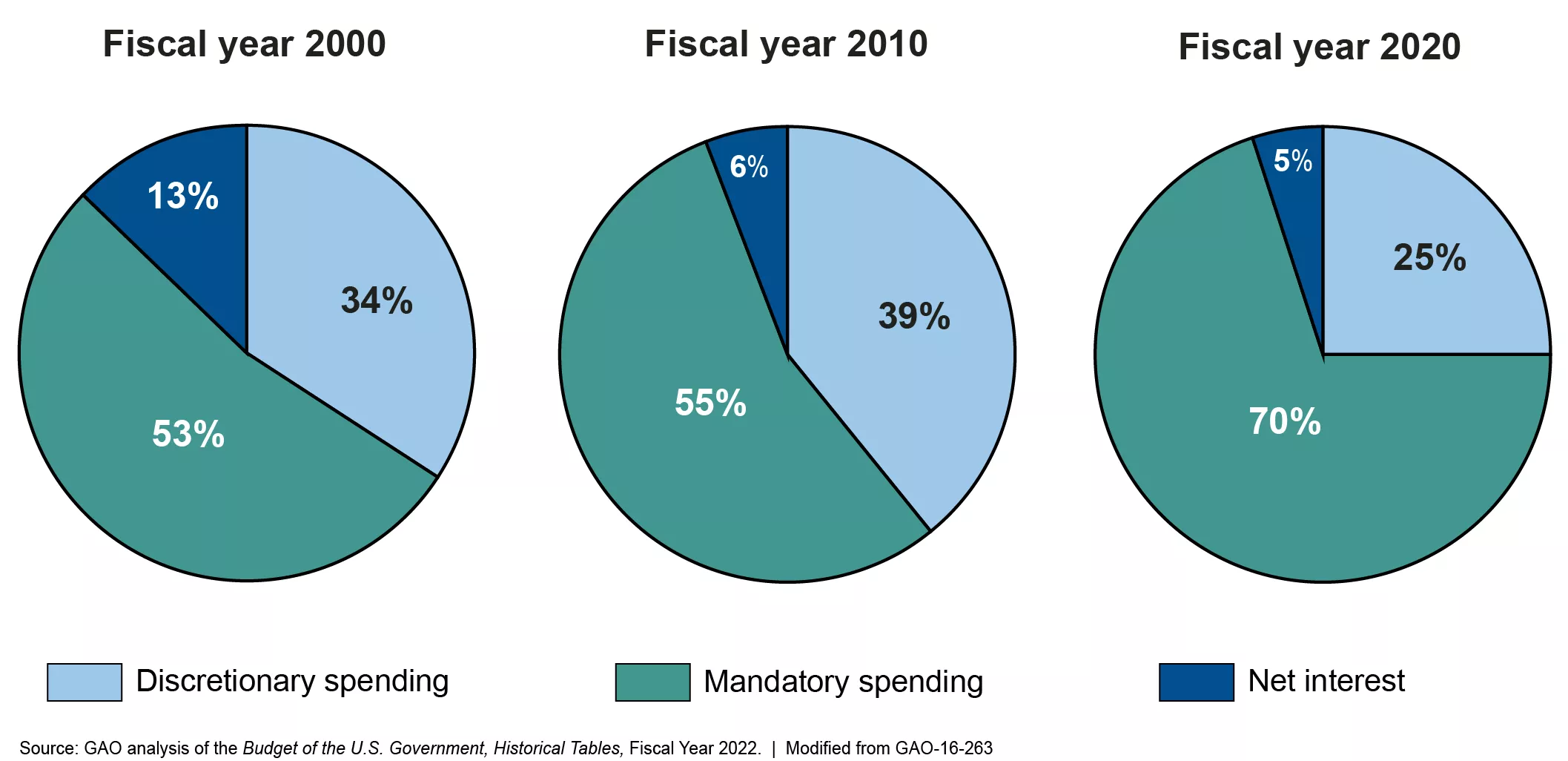

Over the past few decades, mandatory spending has increased compared to discretionary spending. In addition, spending on net interest has recently increased, due to higher levels of federal debt and higher interest rates. The increase in mandatory spending and net interest is projected to continue in the coming years.

Composition of Total Federal Spending

Image

Note: Net interest is primarily interest paid on debt held by the public. It is part of current outlays (spending) by the government and appears as an outlay in the budget.

Given the relative decline in resources for discretionary spending, careful management of agency budgets is vital to ensuring that agencies can continue to effectively achieve their missions and deliver services to the public. For example, U.S. Immigration and Customs Enforcement (ICE) could better plan for future resource needs by updating spending plans and reviewing budget models.

Agencies also face disruptions and ongoing uncertainty in the federal appropriations process. For instance, Congress has enacted continuing resolutions (CRs) in all but 3 of the last 48 years (as of FY 2024) to allow agencies to continue operations until final appropriations decisions are made. Operating under CRs has sometimes resulted in administrative inefficiencies and limited management options in areas such as hiring and travel for the agencies. Agencies have developed strategies to mitigate the possible disruptions from CRs, allowing operations and services to continue. These strategies include using other available sources of funding from multi-year appropriations or delaying the start of grant programs until later in the year.

Other budget issues that federal agencies must navigate include:

- Funding gaps. When appropriations expire and neither new appropriations nor CRs are enacted, a funding gap may occur, and portions of the government may shut down. In FY 2019, the federal government partially shut down for 35 days, which affected 800,000 employees at various federal agencies and delayed about $18 billion in discretionary spending. To help with this process in the future, agencies could make improvements in their shutdown plans and operations.

- Sequestration. Automatic, across-the-board spending reductions to both mandatory and discretionary spending (known as sequestration) were triggered in March 2013 after Congress and the President did not enact required legislation to reduce the deficit. Since 2013, sequestration of mandatory spending has occurred each year, resulting in smaller and delayed direct payments to program beneficiaries, reduced services, and reduced tax credits, among other things. Under current law, sequestration will continue through 2032 for Medicare and 2031 for other mandatory spending. To promote transparency of this process, the Office of Management and Budget could publicly report the actual reductions in budget authority each year as a result of sequestration.

- User fees. Some agencies collect funds through user fees—fees assessed to users for goods or services the federal government provides, such as fees to enter some national parks. Some of these agencies relied on their fee reserves when they experienced revenue instability during the COVID-19 pandemic—and could better plan for future user fee disruptions. Additionally, there is no comprehensive, government-wide data that identifies specific user fees. Such data could help Congress identify trends in collections and significant changes that could be an indication of an agency’s performance.